We believe the world is a better place with community banks and credit unions and that, with Banno, they can bring personal service to their digital channels.

Our problem space

Before the Internet

Before the Internet, community FIs had personal relationships with customers at the counter inside the branch. After a while, employees of the FI would learn your name and a little bit about you. There was coffee, local news and weather, friendly faces, and of course there were suckers for the kiddos. Cross-selling of additional products and services happened with a personal touch.

The branch evolved to include a drive-through window for quicker, more convenient service. Later, ATM networks were created to allow withdrawals and deposits without a teller. Self-service banking was created.

Along came the browser

In the early 90s, Jack Henry created one of the first online banking applications. Self-service banking was now possible at the desk in every home with a dial-up connection and more self-service features, such as bill pay, check capture and new account origination were made possible.

The community FI’s service could not be replicated online, cross-selling was more difficult and less personal. Vendors like JHA gave the FI amazing tools to enable self-service but began the process of systematically destroying their business model.

In the summer of 2007, the first iPhone was released which put faster internet in the hands of millions of people. Banno released its first version of mobile banking in 2011. In this time, banks and credit unions started to consolidate their branches, sometimes reformatting them into stores that focus more on self-service and scheduled appointments.

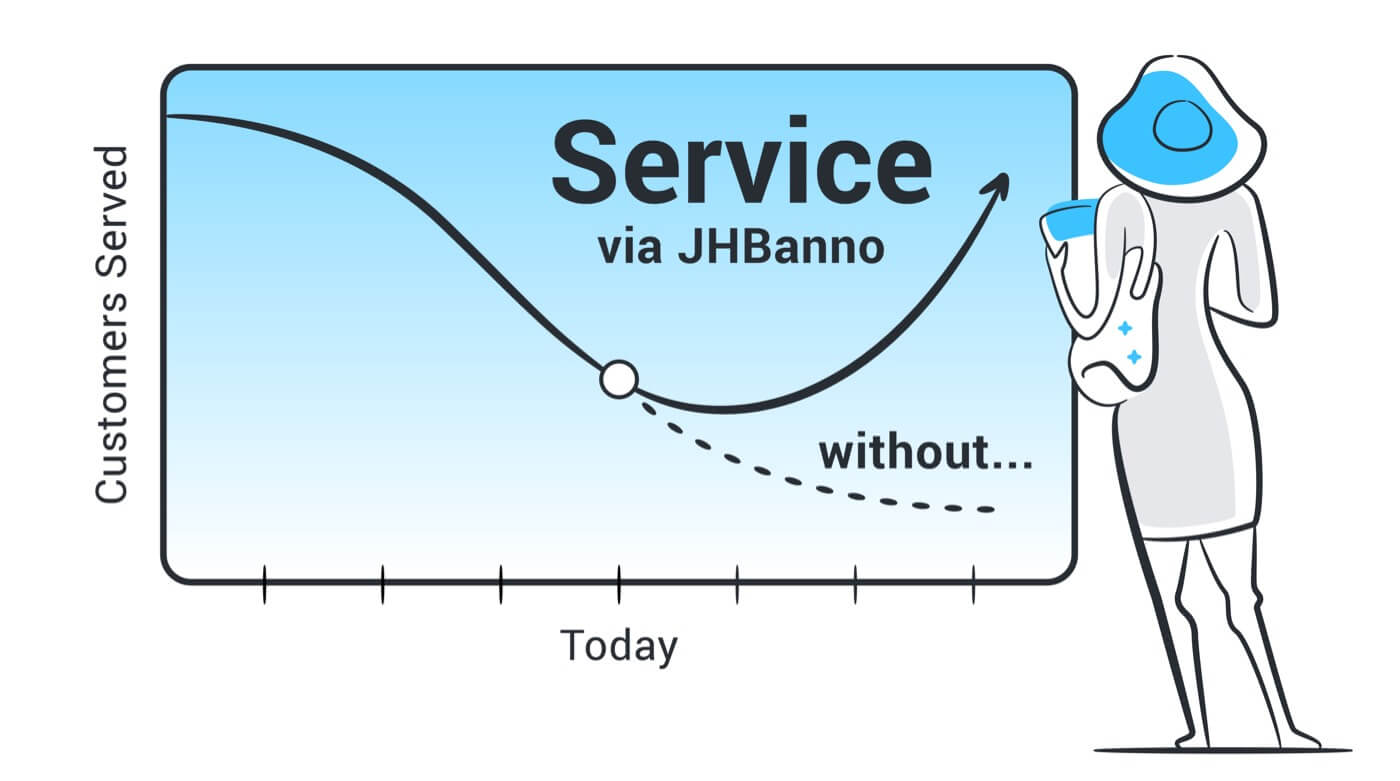

Now, community FIs have to pay for their brick and mortar branches to support their baby-boomer base as well as having to pay for online banking and mobile banking from vendors like JHA to support the internet-native millennials. Digital banking is a cost center, but the FI needs it to attract and retain customers to hold deposits in order to make loans. Adding insult to injury, the community FI doesn’t have the tools to provide world-class service or to cross-sell in the digital space in a cost-effective way.

Banno’s mission

Enable best-in-breed self-service

Having a great digital experience is table stakes. Banno will create the best experience in self-service banking across the digital channels. We will find creative ways of meeting the needs of consumers and small businesses so that they can help themselves.

Create the digital counter

Banno will bring back the counter that was once in the branch to enable community institutions to provide world-class support when self-service hits an edge. Support through the digital channel must be personal and conversational.

Focus on the buying experience

In fintech, the buying experience is typically referred to as account opening. Banno will provide community FIs with tools to effectively and intelligently market to existing customers and prospects and measure the results. We will streamline the process of applying for a new account and remove all barriers.

Transactional data and historical behavior are the backbone to creating innovative new products that fulfill unmet needs for community FIs and their customers.

Summing it up

By focusing on creating the best self-service transactional experience, creating a digital counter for world-class support, and making a delightful buying experience, Banno will help community FIs drive deposits which will contribute to their ability to lend back to consumers and small businesses.